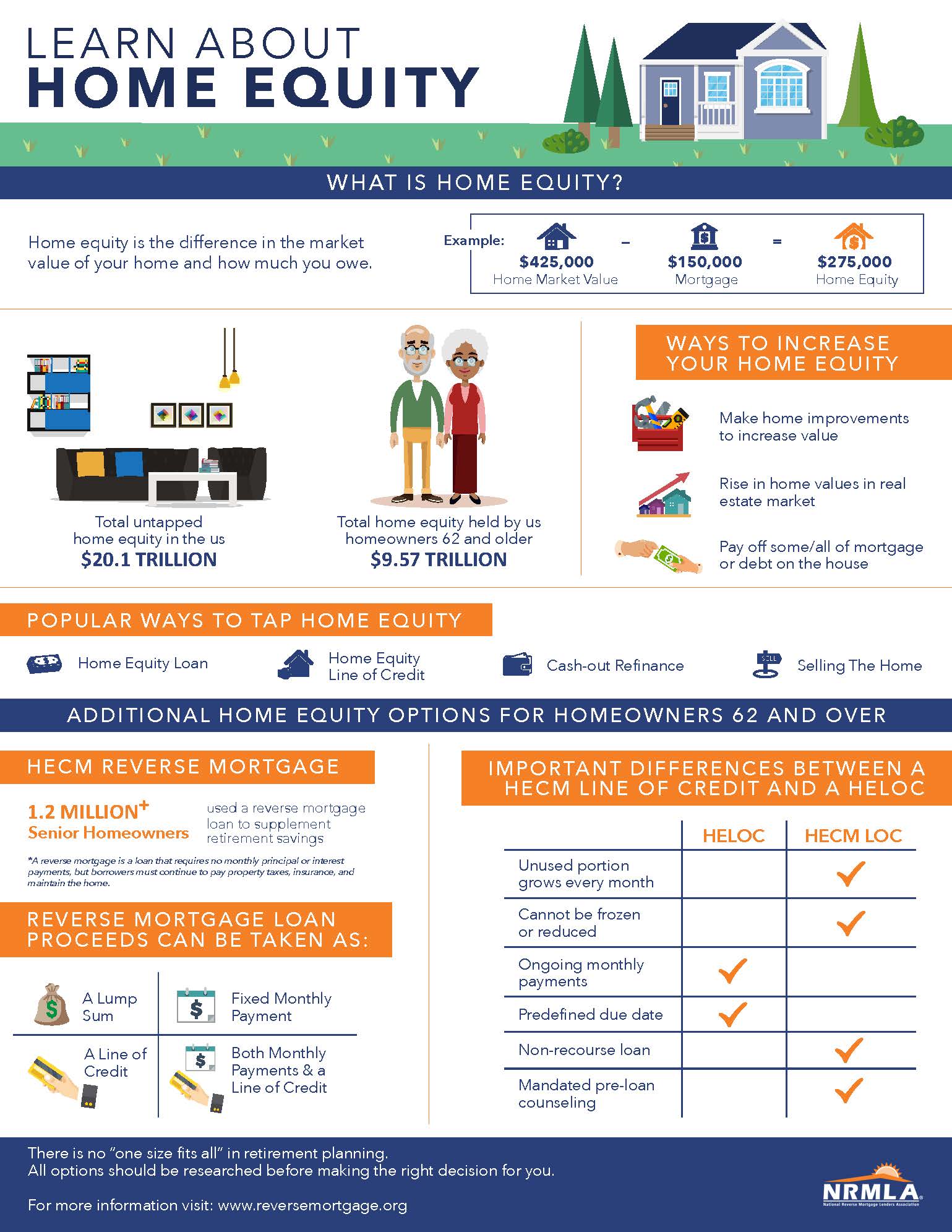

For many homeowners, the equity they have built up in their home is their largest financial asset, typically comprising more than half of their net worth. Yet confusion persists about measuring home equity and the tools available for incorporating it into an overall personal financial management strategy.

The National Reverse Mortgage Lenders Association published “An Introduction to Housing Wealth: What is home equity and how can it be used?” a three-part article that explains home equity and its uses, methods for tapping it, and the special home equity options available for homeowners aged 62 and older. NRMLA also developed the accompanying infographic to help explain home equity and how it can be used.